On February 9, 2022, the US Treasury Department (Treasury) released a report with recommendations for how the Tobacco Tax and Trade Bureau (TTB), Federal Trade Commission (FTC) and Department of Justice (DOJ) can help drive competition in the beer, wine and spirits markets by stepping up conduct enforcement, adopting creative and nuanced theories of harm in merger reviews and implementing new regulations to decrease the burden on smaller industry participants. Treasury’s report is based, in part, on hundreds of comments received from industry participants and paints a detailed picture of the current landscape for alcohol beverage distribution and sale across the United States.

On February 1, 2022, a federal jury found a former engineering firm executive guilty of conspiring to rig bids and defraud the North Carolina Department of Transportation (NCDOT) of hundreds of public works contracts worth more than $23 million. From at least 2009 through fall 2018, Brent Brewbaker was responsible for crafting and submitting bids to NCDOT on behalf of Contech Engineered Solutions LLC, an engineering firm that makes products used in bridge construction, water drainage and other public works projects.

Read more here to learn how companies can minimize the risk that they are investigated by the Procurement Collusion Strike Force (PCSF).

In the United States, antitrust agencies have now filled senior leadership positions, although the Federal Trade Commission (FTC) awaits the appointment of a fifth commissioner. Challenges to mergers continue apace at both the FTC and the Department of Justice (DOJ). The agencies challenged two mergers in the fourth quarter and a third transaction was abandoned. Additionally, nine consent orders were approved. The FTC is also including prior approval provisions in consent orders across industries, requiring parties seeking to settle merger disputes to agree to provide the FTC with greater rights to reject potential future deals.

The European Commission (Commission) imposed interim measures for the first time in the context of the Commission’s determination that Illumina’s acquisition of GRAIL was premature. The Commission conditionally cleared, in Phase I, Veolia’s acquisition of Suez—a transaction involving two French incumbents in the water and waste sectors—following comprehensive commitments. IAG withdrew from its proposed acquisition of Air Europa following the Commission’s decision not to approve the transaction absent further concessions.

In the United Kingdom, the Competition & Markets Authority (CMA) imposed a record fine of £50.5 million on Facebook for breaching an initial enforcement order related to its acquisition of Giphy, and ultimately required Facebook to sell Giphy. The CMA also updated its merger guidance in parallel with the entry into force of the UK National Security and Investment Act, published a new template for initial enforcement orders and updated its guidance on interim measures.

On January 21, 2022, the US Federal Trade Commission (FTC) announced increased thresholds for the Hart-Scott-Rodino Antitrust Improvements Act of 1976 (HSR). The thresholds are indexed to changes in the gross national product (GNP).

NOTIFICATION THRESHOLD ADJUSTMENTS

These increased thresholds are scheduled to be published in the Federal Register on January 24, 2022, which would make them become effective on February 23, 2022. These new thresholds apply to any transaction that closes on or after the effective date:

The base filing threshold, which frequently determines whether a transaction requires the filing of an HSR notification, will increase to $101 million.

The alternative statutory size-of-transaction test, which captures all transactions valued above a certain size (even if the “size-of-person” threshold is not met), will be adjusted to $403.9 million.

The statutory size-of-person thresholds will increase to $20.2 million and $202 million.

The adjustments will affect parties contemplating HSR notifications in various ways. Transactions that meet the current “size-of-transaction” threshold (but not the adjusted $101 million threshold) will only need to be filed if they will close before the new thresholds take effect on February 23, 2022.

Parties may also realize a benefit of lower notification filing fees for certain transactions. Under the rules, the acquiring person must pay a filing fee, although the parties may allocate that fee among themselves. Filing fees for HSR-reportable transactions will remain unchanged; however, the size of transactions subject to the filing fee tiers will shift upward because of the GNP-indexing adjustments:

Filing FeeSize of Transaction $45,000 $101 million, but less than $202 million $125,000 $202 million, but less than $1.0098 billion $280,000 $1.0098 billion or more

In the United States, the US Department of Justice’s (DOJ) challenge of American Airlines and JetBlue’s “Northeast Alliance” after the joint venture’s approval by the US Department of Transportation earlier this year demonstrates the Biden administration’s commitment to aggressive antitrust enforcement. US President Joe Biden issued an Executive Order calling for tougher antitrust enforcement, including “encouraging” the DOJ and Federal Trade Commission (FTC) to modify the horizontal and vertical merger guidelines to address increasing consolidation. At the same time, the FTC, under Chair Lina Khan, continues its rapid pace of change to the merger review process.

Under a new interpretation of Article 22 of the EU Merger Regulation (EUMR), the European Commission (Commission) asserted jurisdiction over Illumina’s acquisition of GRAIL and Facebook’s acquisition of Kustomer, even though the transactions did not meet the Commission or Member State filing thresholds. The EU General Court confirmed a significant gun-jumping fine imposed on Altice for breach of the EUMR notification and standstill obligations.

In the United Kingdom, the UK government published plans to update antitrust rules, including revising its jurisdictional thresholds and expanding the “share of supply” test to allow the CMA to more easily capture vertical and conglomerate mergers, as well as acquisitions of startups. And the Competition & Markets Authority’s (CMA) handling of the Veolia/Suez transaction demonstrates the CMA’s willingness to engage with parties to seek practical interim solutions while it is investigating a consummated transaction for potential antitrust concerns.

In the United States, aggressive antitrust enforcement is likely to continue with the appointment of Lina Khan as Federal Trade Commission (FTC) Chair and the nomination of Jonathan Kanter to lead the Department of Justice’s (DOJ) Antitrust Division. The premerger notification landscape continues to shift as filings reach another record high. Technology companies remain in the “hot seat” as legislators in the US House of Representatives introduced five antitrust reform bills that would change the enforcement landscape for digital platforms, including seeking to preclude large digital platform companies from acquiring smaller, nascent competitors. And the US Department of Justice is making good on President Biden’s pledge to regulate “Big Ag” by challenging Zen-Noh Grain Corporation’s proposed acquisition of 38 grain elevators from Bunge North America, Inc.

Meanwhile, in Q1 2021, the European Commission (Commission) published its Guidance on Article 22 of the EU Merger Regulation. The Guidance encourages the EU Member States to refer certain transactions to the Commission even if the transaction is not notifiable under the laws of the referring Member State(s). In Q2, not long after the issuance of the Guidance, the Commission received its first referral request to assess the proposed acquisition of GRAIL by Illumina. In light of the growing global debate on the need for more effective merger control, EU Competition Commissioner Margrethe Vestager confirmed that the Commission will not soften EU merger policy going forward. The Commission’s statement was made despite the fact no deals have been blocked by the Commission in about the last two years.

President Biden recently issued an executive order affirming his administration’s policy of enforcing the antitrust laws to “combat the excessive consolidation of industry” and cited healthcare markets as one of several priorities. The Federal Trade Commission (FTC) and US Department of Justice (DOJ) already have been actively enforcing the antitrust laws in provider consolidation matters. The FTC is currently challenging the proposed merger of two health systems in New Jersey, and in the past year unsuccessfully challenged the combination of Jefferson Health and Einstein Health in Philadelphia and successfully challenged the proposed combination of two health systems (Methodist Le Bonheur and Saint Francis) in Memphis.

The executive order follows a proposed bill to increase budgets for the FTC and DOJ, FTC resolutions on compulsory process in healthcare investigations, congressional calls to investigate the use of COVID-19 Provider Relief Fund payments for acquisitions, the FTC physician practice acquisition retrospective and other health antitrust developments.

On June 7, 2021, as part of the US Department of Justice’s (DOJ) continuing commitment to prosecuting cases where the government is a victim, a government contractor pleaded guilty to one count of bid-rigging and one count of conspiracy to commit mail and wire fraud in connection with the DOJ’s ongoing investigation into public works contracts for the North Carolina Department of Transportation (NCDOT).

Ohio-based Contech Engineered Solutions LLC (Contech) entered its plea of guilty before a federal judge in the US District Court for the Eastern District of North Carolina and was sentenced to pay a $7 million criminal fine. Contech was also ordered to pay an additional $1,533,988 in restitution to the NCDOT. Notably, the DOJ did not impose a term of probation on Contech because Contech agreed to improve its compliance program to prevent recurrence of anticompetitive conduct. Contech, however, is required to cooperate with the DOJ, including producing documents and making witnesses available for interviews or testimony.

Contech and its former executive were indicted in October 2020 on six counts of alleged bid-rigging, conspiracy to commit fraud and mail and wire fraud in connection with a decade-long conspiracy involving public works projects in North Carolina.

This prosecution highlights the DOJ’s ongoing commitment to the Procurement Collusion Strike Force (PCSF) and its efforts to scrutinize public procurements and combat collusion and related fraud in government contracting.

The PCSF has conducted extensive training of law enforcement officers and procurement officers, among others, to help identify scenarios and situations where collusion is more likely to occur. The PCSF is also utilizing data analytics to advance its investigations, building on technological advancements and more useable data sets to target and prosecute anticompetitive conduct.

Importantly, the PCSF has recently doubled in size and has gone global just as the United States has approved unprecedented stimulus spending in response to the global COVID-19 pandemic and as the Biden administration is poised to approve a new infrastructure plan. The PCSF has provided tools that allow any individual to report suspected collusion via email or an online tip center. Enforcers’ renewed commitment to procurement collusion—coupled with increased government spending—will likely lead to more investigations and additional prosecutions in 2021.

Contech, a manufacturer of aluminum and other products, conspired with its supplier in bidding on numerous NCDOT public works projects. According to the indictment, the former Contech executive would obtain (or direct his subordinate to obtain) the supplier’s total bid price in advance. Using that information, Contech then submitted bids to be intentionally higher than its supplier. The indictment also alleged that Contech submitted false certifications that its bids were competitive and free of collusion throughout the conspiracy.

The indictment alleged bid-rigging between a manufacturer and its supplier, which is typically a vertical relationship and generally subject to the Rule of Reason rather than per se criminal analysis. Under the Rule of Reason, antitrust enforcers balance the anticompetitive effects of the conduct in question against the procompetitive benefits. Certain anticompetitive conduct, however, [...]

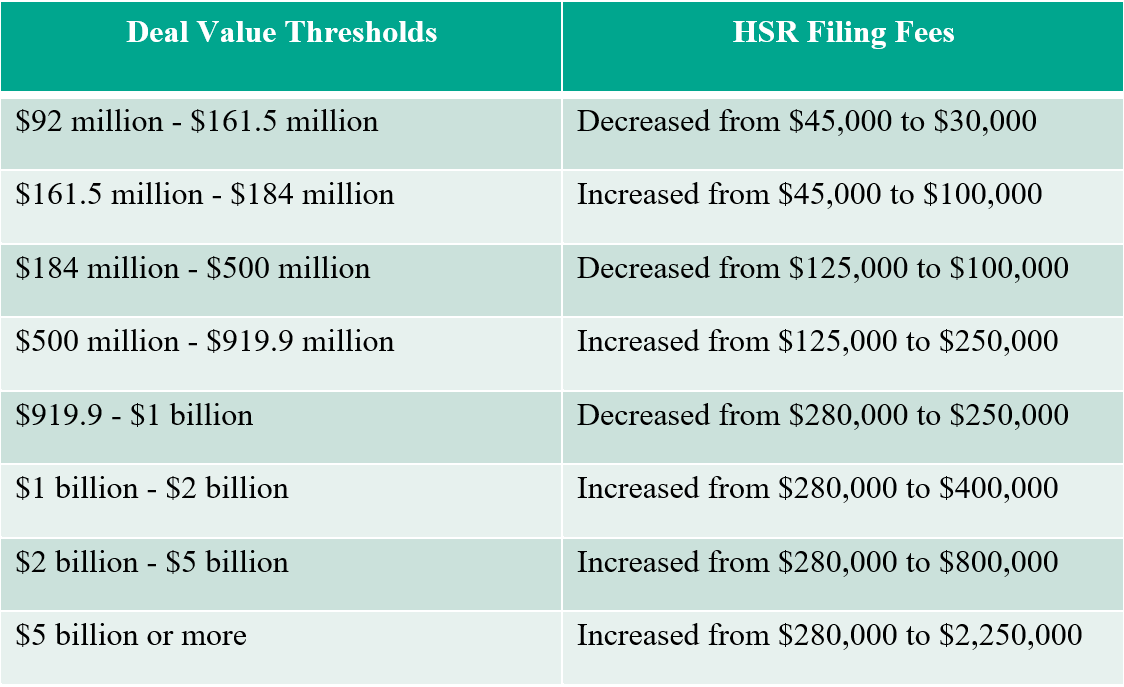

On June 6, 2021, the US Senate passed the Merger Filing Fee Modernization Act of 2021. The bill is co-sponsored by Senator Amy Klobuchar (D-MN), the Chairwoman of the Senate Subcommittee on Antitrust, Competition Policy and Consumer Rights; and Senator Chuck Grassley (R-IA).

The bill amends the premerger notification provisions of 15 U.S.C. § 18a and substantially increases the Hart-Scott-Rodino Act (HSR) filing fees for large mergers, while also effectuating a slight decrease in HSR filing fees for smaller mergers. The text of the bill can be found here.

The adjusted HSR filing fees are as follows:

The proposed HSR filing fees are subject to annual increases based on the Consumer Price Index (CPI), unless the CPI increase is less than 1%. Any changes must be published by the Federal Trade Commission (FTC) each year (no later than January 31). The HSR filing fee thresholds themselves will remain correlated to Gross National Product (GNP).

The competition agencies also stand to directly gain from the passage of this bill. Section 3 of the bill authorizes the appropriation of increased funds for both the Department of Justice Antitrust Division (DOJ) and the FTC. The bill appropriates $252 million to the DOJ and $418 million to the FTC, substantially increasing the resources at the disposal of the regulatory agencies and even exceeding the FTC’s requested budget for FY 2022.

The bill is still subject to approval in the House of Representatives and by President Biden. But given the bipartisan support for this bill, its passage appears likely, and it raises the potential for additional bipartisan antitrust legislation in the future.

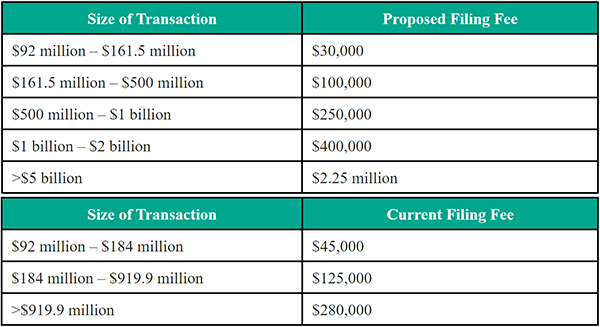

On Thursday, May 13, the US Senate Judiciary Committee voice-vote approved and advanced Senator Amy Klobuchar’s (D-MN) Merger Filing Fee Modernization Act of 2021. This bill seeks to increase HSR filing fees required for mergers and acquisitions, altering fees for all transactions, and substantially increasing HSR filing fees for deals greater than $5 billion to $2.25 million. HSR filing fees have not been updated since 2001.

The proposed bill would further increase the fees each year in accordance with the Consumer Price Index. In an effort to gain bipartisan support, the bill would decrease filing fees for smaller transactions, while increasing fees significantly for all deals over $500 million. Below are tables showing the proposed HSR filing fees versus the current HSR filing fees based on transaction size.

Although no changes are imminent, the advancement of this bill indicates politicians’ continued focus on increasing the burden on mid-size and larger companies seeking to merge, while slightly reducing fees for smaller transactions.Senator Klobuchar has argued that the substantial increase in fees for larger deals is needed because of the government cost required to investigate larger deals. Further, she said she believes the affected parties, such as major technology companies, could easily handle the cost because it is a small expense compared to the amount these companies often spend on legal and professional support in effectuating the deals.

Subscribe

Subscribe